AI in Commercial Auto Insurance: Smarter Risk Assessment

The commercial auto insurance industry faces a serious profitability crisis. Nine of the top ten US commercial auto carriers lost money in 2025, spending $107 on claims and expenses for every $100 collected in premiums. Nuclear verdicts — liability claims exceeding $10 million — compound the problem further, with just 16 such verdicts totaling $1.3 billion in 2025 alone. Traditional underwriting methods, built on static demographic data and historical loss tables, simply cannot keep pace with the complexity of today’s risk environment.

Artificial intelligence is changing that equation — and changing it fast. Across underwriting, pricing, claims processing, and fraud detection, AI gives commercial auto insurers the tools to shift from reactive risk management to predictive risk prevention. This article examines how that transformation works in practice, how leading insurers like biBERK and Progressive apply AI within the commercial auto space, and what businesses need to understand to navigate this new landscape effectively.

Table of contents

Quick Summary

| AI Application | What It Does | Business Impact |

|---|---|---|

| Predictive underwriting | Analyzes driver behavior, fleet data, and loss history | More accurate pricing; reduced adverse selection |

| Telematics & usage-based pricing | Real-time monitoring of speed, braking, mileage | Behavior-linked premiums; safer fleets |

| AI claims processing | Automates triage, damage assessment, fraud flagging | Faster settlements; lower loss ratios |

| Natural language processing | Reads applications, contracts, and loss run documents | Faster submission review; fewer manual errors |

| Fraud detection | Identifies claim anomalies against historical patterns | Reduced non-productive claim expenses |

| Real-time crash detection | Detects collisions via smartphone sensors; initiates claims | Faster response; improved customer experience |

Key figures: 88% of US auto insurers currently use, plan to use, or plan to explore AI/ML models in operations (NAIC, 2025). The telematics-based auto insurance market is projected to grow at a 16.52% CAGR from 2025 to 2035.

How Are biBERK and Progressive Reshaping AI-Driven Commercial Auto Insurance?

Two companies stand out in the US commercial auto insurance market for their distinct approaches to AI-enabled risk management: biBERK and Progressive. Both carriers actively use technology and data to improve the commercial auto insurance experience — but they serve different market segments and apply AI in meaningfully different ways.

What makes biBERK’s approach to commercial auto insurance distinctive?

biBERK is a Berkshire Hathaway company founded in 2015 with a clear mission: make commercial insurance as simple and affordable as possible for small businesses. The company serves over 500,000 customers and brings 75+ years of Berkshire Hathaway underwriting experience to a fully digital, direct-to-business platform. For small business owners buying commercial auto insurance — contractors, delivery services, landscapers, transportation companies — biBERK offers a streamlined three-step online process that delivers instant quotes and immediate coverage without requiring an agent or broker.

The platform’s automated underwriting engine reflects AI-informed risk logic built on Berkshire Hathaway’s deep actuarial data pool. Rather than routing small commercial accounts through a complex manual underwriting process, biBERK’s technology evaluates applicants against risk profiles derived from decades of claims and loss data — and returns a quote within minutes. This approach allows biBERK to offer savings of up to 20% compared to traditional channels, because the technology eliminates much of the manual overhead that drives up premium costs.

How does Progressive lead the commercial auto insurance industry in AI investment?

Progressive operates at a fundamentally different scale. With an ICT spend of $2.2 billion in 2022 and AI systems embedded across its entire value chain, Progressive represents arguably the most advanced application of AI in US auto insurance. Its Snapshot telematics program — powered by machine learning and big data analytics — has collected nearly two decades of behavioral driving data that now feeds the company’s risk pricing models directly.

For commercial auto customers specifically, Progressive offers Smart Haul and Snapshot ProView — usage-based insurance (UBI) programs that give fleet operators behavior-linked pricing and safety insights. Beyond pricing, Progressive’s AI drives claims efficiency: adjusters using AI-assisted estimation tools complete 2.5 times more estimates per day, contributing to approximately 15% faster end-to-end claims cycle times. The results confirm the strategy’s strength — a combined ratio of 86.0 in Q1 2025, 17% net premiums written growth, and 18% policy-in-force growth year-over-year.

How do biBERK and Progressive compare on AI-driven commercial auto features?

| Feature | ||

|---|---|---|

| Target market | Small businesses | Small to large commercial fleets |

| Online quote speed | Minutes; fully self-service | Minutes to hours depending on fleet size |

| AI underwriting | Automated digital underwriting engine | ML-powered multi-variable risk models |

| Telematics program | Not publicly offered | Smart Haul, Snapshot ProView (commercial UBI) |

| Claims AI | Digital claims filing; phone support | AI-assisted damage estimation (2.5x productivity) |

| Crash detection | Not available | Accident Response (AI + CMT DriveWell Fusion, launched Nov 2024) |

| Fraud detection | Berkshire Hathaway data backing | ML anomaly detection; H2O.ai partnership |

| Generative AI | Automated quoting logic | Gen AI for pricing refinement and marketing |

| Financial strength (AM Best) | A++ | A+ |

| Available states (commercial auto) | 21 states | Nationwide |

| Savings vs. traditional channels | Up to 20% | Behavior-based discounts (avg. $322/policy via Snapshot) |

Both carriers bring genuine AI-driven value to commercial auto buyers. biBERK excels in accessibility and simplicity for small businesses. Progressive leads on telematics depth, claims technology, and commercial fleet tools.

Why Is Traditional Risk Assessment No Longer Enough for Commercial Auto?

What limitations does conventional underwriting create for businesses?

Traditional commercial auto underwriting relies on static inputs: vehicle type, driver demographics, ZIP code, years in business, and historical loss runs. These factors describe what happened in the past — but they say very little about what will happen next. A delivery driver with a clean three-year record might be developing dangerous habits that no static report captures. A fleet operator in a growing market might face different risks than the historical data from a comparable but different geography suggests.

Furthermore, the claims environment has shifted dramatically. Nuclear verdicts — liability awards exceeding $10 million — now pose an existential risk to commercial auto insurers. In 2024, just 16 such verdicts totaled $1.3 billion, averaging $81 million per claim. Static risk assessment cannot flag the behavioral patterns that precede catastrophic claims. As a result, carriers that rely on traditional underwriting alone consistently price risk incorrectly, leading to loss ratios that erode profitability across entire books of business.

How does AI change what insurers can measure and predict?

AI fundamentally expands the data available to underwriters. Instead of relying only on static applicant information, AI systems analyze behavioral signals, vehicle sensor data, environmental conditions, and claims patterns simultaneously. This shift enables insurers to move from a “detect and repair” model — paying claims after losses occur — to a “predict and prevent” model that identifies risk before it materializes.

According to the NAIC, 88% of US auto insurers currently use, plan to use, or plan to explore AI and ML models in their operations. McKinsey estimates that AI technologies could add up to $1.1 trillion in potential annual value for the global insurance industry. Critically, that value comes not just from efficiency gains, but from better risk selection — writing the right risks at the right price.

How Does AI-Powered Underwriting Actually Work in Commercial Auto?

What data sources does AI-driven underwriting analyze?

Modern commercial auto underwriting AI draws on a wide range of structured and unstructured data sources. The most impactful include:

- Telematics data: Speed, braking patterns, acceleration, time of day, route choices, and miles driven — all captured in real time via OBD devices, smartphones, or in-vehicle sensors

- Loss run history: Claims records from previous carriers, analyzed for frequency, severity, and cause patterns

- Vehicle data: Make, model, safety ratings, age, and installed safety features

- Driver records: MVR data, licensing history, and prior incidents

- Business data: Industry type, years in operation, fleet size, geographic operating area

- External signals: Natural language processing (NLP) analyzes business websites, financials, and public records to identify risk factors such as contractor violations or litigation exposure

By combining these inputs, AI models surface correlations that human underwriters would miss across thousands of individual risk variables. Progressive‘s hybrid ML models, for instance, blend classical generalized linear models with neural networks to analyze complex, high-dimensional telematics data vectors — enabling the system to discover non-linear relationships between driving behavior and claim likelihood.

What does usage-based insurance mean for commercial fleet operators?

Usage-based insurance (UBI) represents the most direct application of telematics AI to commercial auto pricing. Rather than paying a flat premium based on historical demographics, fleet operators pay premiums that reflect their actual driving behavior — rewarding safe driving with lower costs and flagging risky patterns before they result in claims.

For commercial customers, Progressive offers two primary UBI programs:

- Smart Haul: Designed for owner-operators and small trucking fleets, this program uses electronic logging device (ELD) data to measure mileage and driving behavior, offering premium adjustments tied directly to real fleet performance

- Snapshot ProView: A fleet telematics program that provides both pricing benefits and driver safety coaching tools, helping fleet managers identify their highest-risk drivers and intervene proactively

The commercial value of these programs extends beyond premium savings. Fleet operators who use telematics gain visibility into driver behavior they previously lacked, enabling coaching conversations backed by data rather than anecdote.

How Is AI Transforming Commercial Auto Claims Processing?

What does AI bring to claims handling that traditional methods cannot?

Claims processing is where AI delivers some of its most measurable ROI in commercial auto insurance. Traditional commercial claims handling involves significant manual work: reviewing incident reports, assessing damage, coordinating with repair shops, and validating coverage details. AI accelerates and improves nearly every step of that process.

Progressive’s implementation offers the most data-rich example available. Adjusters using AI-assisted damage estimation tools complete 2.5 times more estimates per day compared to manual methods — and the overall end-to-end claims cycle runs approximately 15% faster. The full rollout of these capabilities in 2025 allowed Progressive to handle growing claims volume without hiring an estimated 200 additional staff members in 2025 — a direct, quantifiable cost saving that feeds directly into underwriting profitability.

How does AI detect and reduce commercial auto fraud?

Fraud represents a significant cost driver across commercial auto lines. AI fraud detection works by comparing incoming claims against historical data patterns, flagging anomalies that human adjusters might miss across large claim volumes. Machine learning models identify signatures of fraud — unusual claim timing, inconsistent injury reports, implausible damage profiles — and route suspicious claims for enhanced review before payment.

Progressive’s partnership with H2O.ai supports ML-based fraud detection that has contributed to a 14% reduction in non-productive claim expenses. For commercial auto — where a single fraudulent large-loss claim can distort loss ratios across an entire account — this kind of proactive fraud flagging delivers outsized value compared to personal auto lines.

What Does AI-Powered Crash Detection Mean for Commercial Auto Policyholders?

How does real-time crash detection change the claims experience?

In November 2025, Progressive launched Accident Response — an AI-driven crash-detection service built in partnership with Cambridge Mobile Telematics (CMT). The system uses CMT’s DriveWell Fusion platform, which aggregates data from smartphone sensors and in-vehicle devices to detect collisions in real time.

When the platform detects a likely crash, it automatically reaches out to the driver through the Progressive app, offering towing services, emergency response, and immediate claims filing support. If the driver doesn’t respond, the system triggers a follow-up call. This approach compresses the first-notice-of-loss (FNOL) timeline from days to minutes — and in some cases, from minutes to seconds.

For commercial fleet operators, the implications are significant:

- Drivers receive immediate support at the moment they need it most

- Fleet managers get faster notification of incidents involving company vehicles

- Claims open faster, with more accurate initial data captured at the scene

- Injury triage and emergency response happens before the situation worsens

The global insurance telematics market reached $6.8 billion in 2025 and is forecast to grow at an 18.9% compound annual growth rate through 2034 — indicating that real-time crash detection and AI-driven claims initiation will become standard features across the market, not just differentiators for leading carriers.

How Does AI Address the Commercial Auto Profitability Crisis?

Why did so many commercial auto carriers lose money in 2026?

The commercial auto loss picture in 2026 was stark. Nine of the top ten US commercial auto carriers spent more than they collected — a combined ratio above 100% across most of the industry. Three interconnected factors drove that outcome:

- Nuclear verdicts: Large-loss liability claims, often exceeding $10 million, wiped out underwriting profits on entire portfolios. Traditional risk models failed to identify which drivers and fleets carried the behavioral patterns preceding catastrophic claims.

- Adverse selection: Carriers without strong risk segmentation attracted higher-risk fleets because they couldn’t price accurately enough to distinguish between safe and dangerous operators.

- Inflation: Repair costs, medical expenses, and legal settlements all rose faster than premium adjustments could absorb.

How does better AI risk segmentation solve this problem?

Superior risk segmentation — knowing which risks to write and at what price — separates profitable commercial auto carriers from unprofitable ones. AI enables this segmentation in ways that static models cannot.

Progressive‘s AI-driven approach delivers 9% more accurate risk pricing, according to available research. That accuracy advantage allows Progressive to offer lower premiums to safe drivers — attracting and retaining the most profitable segment of the market — while correctly pricing or declining higher-risk accounts. The outcome shows in the numbers: a combined ratio of 86.0 in Q1 2025, well below the industry average that saw most carriers losing money.

For small business owners buying commercial auto through platforms like biBERK, AI-powered underwriting delivers a different but equally important benefit: accurately priced coverage for low-risk operators who would otherwise overpay under crude demographic-based models. biBERK’s automated underwriting engine, backed by Berkshire Hathaway’s actuarial depth, applies this logic at scale — delivering savings of up to 20% for qualified small business accounts.

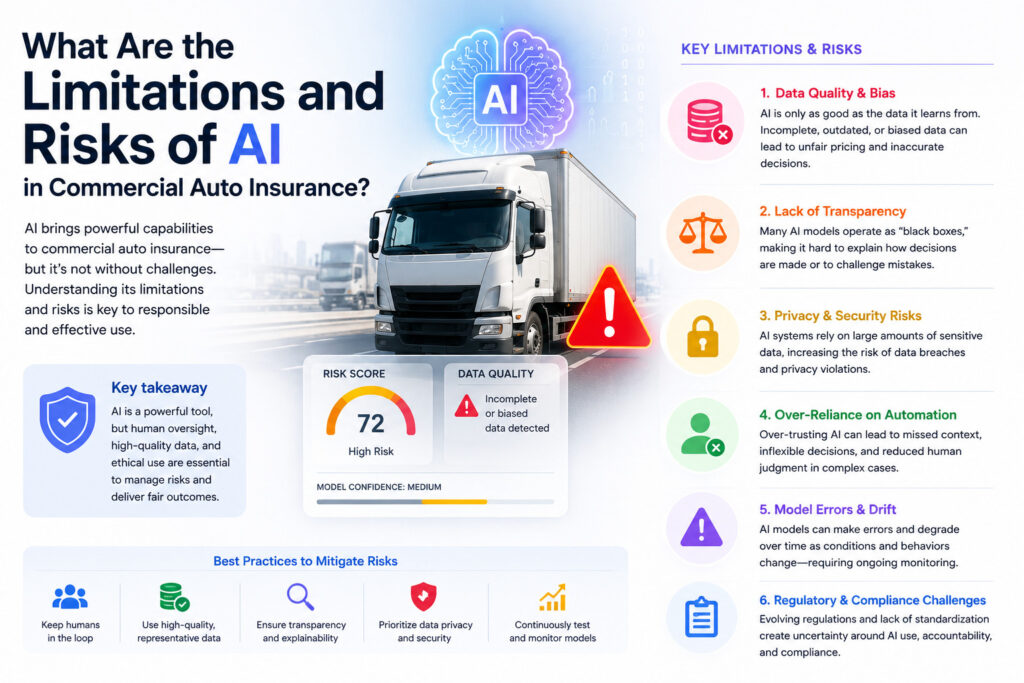

What Are the Limitations and Risks of AI in Commercial Auto Insurance?

Where does AI in commercial auto insurance still fall short?

AI is transforming commercial auto insurance — but it isn’t solving every problem. Several important limitations deserve acknowledgment:

| Limitation | Detail |

|---|---|

| Data quality dependency | AI models are only as good as the data they train on; poor data produces poor predictions |

| Regulatory complexity | The EU AI Act (2025) and US state-level regulations impose transparency and fairness requirements on AI insurance models |

| Complex bespoke risks | Highly specialized commercial risks — multinational logistics firms, specialized cargo haulers — still require human underwriters with deep domain knowledge |

| Bias risk | AI models trained on historical data can encode historical biases; regulators are actively developing oversight frameworks |

| Telematics privacy | Drivers and fleet operators raise legitimate concerns about continuous behavioral monitoring |

| Smaller carrier gap | Carriers without large ICT budgets ($2.2B+) cannot replicate leading insurers’ AI infrastructure without strategic partnerships |

The regulatory environment is evolving rapidly. As of March 2026, the NAIC’s Big Data and AI Working Group is piloting an AI Systems Evaluation Tool across 12 states, with full adoption anticipated at the 2026 Fall National Meeting. Insurers that build AI-aware compliance practices today will avoid the reactive scramble that less-prepared carriers face as oversight tightens.

Why Should Small Businesses Choose biBERK for Commercial Auto Insurance?

What specific advantages does biBERK deliver for small business owners?

Throughout this article, biBERK — Auto Insurance US has appeared as the most accessible entry point for small businesses seeking AI-informed commercial auto coverage. Several factors make the platform particularly compelling for this audience:

- Instant digital coverage: The fully online quote-to-bind process takes minutes, removing the friction of broker appointments and paper applications

- Berkshire Hathaway financial strength: biBERK policies carry an A++ AM Best rating — the highest possible — giving policyholders confidence in claims-paying capacity

- Up to 20% savings: The automated underwriting platform eliminates agent commissions and manual overhead, passing savings directly to policyholders

- Small business specialization: biBERK exclusively serves small businesses, meaning its coverage structures, limits, and pricing are designed around the actual needs of owner-operators rather than large corporate accounts

- Coverage for a wide range of vehicles: Cars, vans, trucks, trailers, and specialized commercial vehicles all qualify for coverage, making biBERK practical across industries from construction to food delivery to consulting

biBERK currently offers commercial auto insurance in 21 states, with ongoing expansion. For small business owners in covered states, getting a quote from biBERK represents one of the fastest paths to affordable, technology-driven commercial auto coverage backed by one of the world’s most financially stable insurance organizations.

Conclusions: Is AI in Commercial Auto Insurance Delivering Real Value?

The evidence is clear and growing: AI genuinely improves commercial auto insurance — for carriers and policyholders alike. For insurers, AI enables more accurate risk pricing, faster claims resolution, proactive fraud detection, and the kind of superior risk segmentation that separates profitable carriers from unprofitable ones. Progressive‘s 86.0 combined ratio in Q1 2025, achieved in a market where most competitors lost money, demonstrates what AI-driven underwriting discipline can accomplish at scale.

For businesses, the AI transformation means fairer premiums, faster claims, and access to coverage programs that reward safe driving behavior rather than penalizing entire industries based on aggregate historical loss data. Additionally, platforms like biBERK — Auto Insurance US make this technology accessible to small businesses that previously had no practical path to sophisticated, data-driven commercial coverage. With instant online quoting, Berkshire Hathaway financial strength, and savings of up to 20%, biBERK offers small business owners the benefits of AI-powered underwriting without requiring large-enterprise resources.

The road ahead holds even more transformation. Pipedrive’s 2025 roadmap suggests agentic AI systems will increasingly automate multi-step underwriting workflows. The NAIC’s regulatory framework, expected to reach full adoption in late 2026, will bring greater transparency requirements that push carriers toward explainable AI models. And as telematics adoption crosses from pilot programs to mainstream deployment — with the market forecast to grow at 16.52% annually through 2035 — real-time behavioral data will become the default foundation of commercial auto pricing rather than a premium add-on.

Businesses that understand this shift, invest in the right technology partnerships, and select carriers that apply AI thoughtfully will find themselves better protected, more accurately priced, and more resilient in a claims environment that continues to grow more complex and costly.

Frequently Asked Questions

AI-driven underwriting can reduce costs for small businesses — but the outcome depends on the business’s risk profile and the data it provides. Carriers like biBERK pass technology savings to policyholders through streamlined digital platforms, advertising savings of up to 20% compared to traditional agent-distributed insurance. For fleets using telematics programs like Progressive‘s Smart Haul or Snapshot ProView, safe driving behavior translates directly into premium reductions — with Snapshot participants saving an average of $322 per policy at renewal. Conversely, AI also enables more precise pricing for higher-risk operators, which means businesses with poor safety records or high loss histories may see premiums that more accurately reflect their actual risk than they would under blunter demographic models.

Commercial auto insurers use telematics data to measure driving behavior — specifically speed, braking frequency, acceleration patterns, time of day, and mileage. This data feeds directly into usage-based insurance (UBI) programs that link premium calculations to actual fleet performance rather than historical demographics. Participation in telematics programs is generally voluntary for commercial policyholders, and carriers disclose upfront how the data affects pricing. Progressive, for instance, explicitly informs commercial customers that Snapshot data can result in either premium reductions or increases depending on recorded behavior. Businesses that opt out of telematics typically pay standard actuarially rated premiums rather than behavior-based ones. For fleet operators with demonstrably safe driving records, opting into telematics almost always delivers net financial benefit.

How Does Partnering with Solution for Guru Improve Your Insurance Technology Strategy?

What does Solution for Guru bring to businesses navigating AI-driven insurance tools?

As AI reshapes commercial auto insurance, businesses face a new challenge: understanding and managing the technology layer that now sits between their operations and their coverage. Fleet management systems, telematics integrations, CRM tools, and insurance portals all generate data that affects risk profiles, premium calculations, and claims outcomes. Managing that ecosystem effectively requires expertise that most small and mid-sized businesses don’t have in-house.

Solution for Guru is a technology consulting firm that helps businesses build and optimize the operational infrastructure that underpins smarter insurance management. Working with Solution for Guru delivers concrete advantages for businesses that want to make the most of AI-driven commercial auto insurance programs:

- Technology integration: Solution for Guru connects fleet management tools, telematics platforms, and business operations systems so data flows cleanly between them — ensuring that the behavioral data feeding into insurer AI models accurately reflects your fleet’s actual performance

- Data strategy: AI-driven insurers reward businesses that present clean, consistent, well-organized operational data. Solution for Guru helps structure your business data so it tells the best accurate story to underwriting algorithms

- Ongoing optimization: As your fleet grows, your routes change, and your risk profile evolves, your technology setup should evolve alongside it. Solution for Guru provides the ongoing support that keeps your operational systems aligned with your insurance strategy

In short, Solution for Guru bridges the gap between the AI-driven underwriting tools that insurers like biBERK and Progressive deploy, and the operational reality of running a business with commercial vehicles. The companies that extract the most value from AI-powered insurance programs are those with clean data, well-documented safety practices, and integrated technology stacks — precisely the outcomes Solution for Guru is built to deliver.

Recommended

- Understanding biBERK’s Claims Process for Commercial Auto Insurance

- When Is Progressive More Expensive Than Regional Commercial Auto Insurers?

- Top Progressive Discounts Small Business Owners Should Know About

- 24/7 Policy Management: How Progressive Supports Busy Business Owners

- Is biBERK a Good Choice for Small Business Owners?

- Checklist: Documents Needed for Commercial Auto Insurance

- How Food Truck Owners Can Benefit from Commercial Auto Insurance

- Commercial vs. Personal Auto Insurance: What’s the Difference?

- biBERK vs Progressive Commercial Auto Insurance: Which Is Better?

- Digital Transformation in Commercial Auto Insurance: What’s Next for Businesses?

- Insurance Needs for Contractors with Company Vehicles: What Do You Really Need?

- Commercial Auto Insurance for Delivery Businesses: Why biBERK Is a Strong Option

- What It’s Like to Work in Commercial Auto Insurance (And How to Start)